Latest

Going Local for Supplies Sparks New Frac Sand Boom

Article originally posted in the Financial Times on December 6th, 2017

Written by: Gregory Meyer

Windblown dunes in west Texas are the latest front in the shale oil industry’s campaign to extract more barrels at less cost.

The industry is excavating dunes for frac sand, which is pumped into wells to crack open rocks and get oil and gas flowing. The deposits are in demand because they lie close by the hot Permian shale region, making them cheaper than sands carried in from older mines 1,000 miles away.

Locally dug sand is influencing the economics of US oil production, helping shale supplies compete in world markets. It is also worrying investors who own shares in railroads that haul sand and in sand miners that may be on the cusp of a glut.

Sand was a critical ingredient of the shale drilling revolution. Without it, US oil production would not have nearly doubled in the past decade to an estimated 9.7m barrels per day.

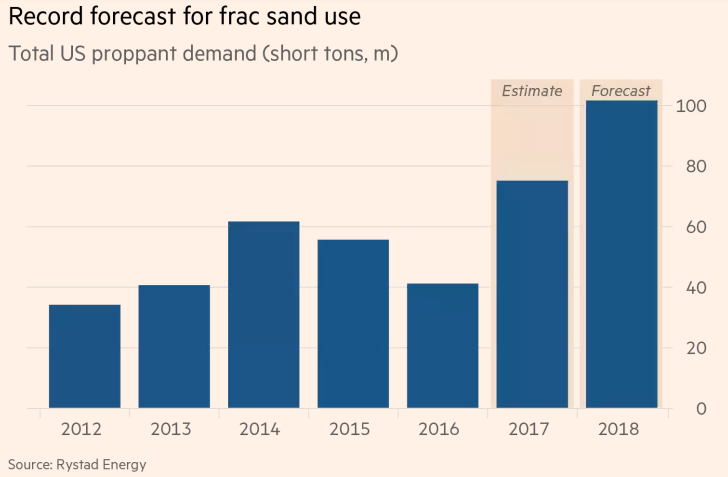

Between 2012 and 2014, total US demand for “proppants” such as frac sand rose from 34m to 61.5m short tons, according to Rystad Energy, a consultancy. Then oil prices collapsed, bringing down sand consumption as well.

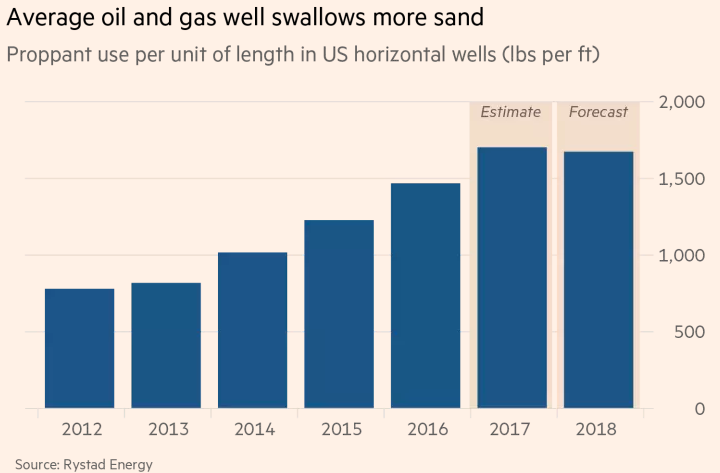

Volumes are again on the upswing as drilling accelerates, oil wells get longer and more sand is used per foot of well. Demand is forecast to surpass 100m short tons next year, Rystad says.

“Right now, the market is really stretched thin,” says Thomas Jacob, a senior analyst at IHS Markit, a research company. “Everyone is running at full capacity.”

But this sand boom is different than the last. In the first phase of the shale fracking boom, oil producers were notorious for prioritizing production growth over investor returns.

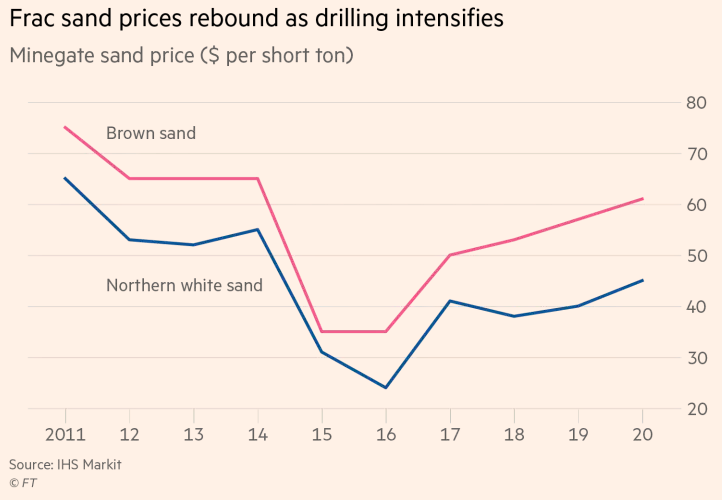

They sought premium sand supplies far from the oil patch in states such as Wisconsin. Its “northern white sand” was prized for hardness and roundness that made a porous latticework inside underground wells.

But given its bulk, it also cost a fortune to ship. Northern white sand has averaged $41 per short ton at the mine gate this year, according to IHS Markit, but can cost $120 at a Texas well head after transport.

Cost-cutting among oil companies sparked a search for supplies lying around the Permian, known as brown sand. While finer in grain, it is also cheaper at $75-$80 per short ton at the well head, Mr Jacob says. Distances are short enough to make some deliveries economical by truck.

Sand supplier Hi-Crush Partners recently opened a sand mine at Kermit, Texas, with annual capacity of 3m short tons per year. This month, US Silica expects to open a site in Crane county, Texas, that will add about 4m short tons of capacity. A third company, Fairmount Santrol, plans to open a 3m short ton plant in Kermit in 2018.

The shifting sand market has unnerved investors in railroads. At Union Pacific, the largest listed railroad company, frac sand accounts for 5 per cent of revenue, according to Bernstein Research.

Robert Knight, Union Pacific chief financial officer, told a conference last week that brown sand “may well be trucked to the ultimate location rather than rail”, though sand was only a small portion of his railroad’s traffic.

The local sand mines face obstacles to growth. One is the dunes sagebrush lizard, a threatened reptile that lives in the area. Further sand mining threatens to put it on the endangered species list, potentially hobbling oil and gas drilling in the Permian region.

Sand also needs to be washed before it is used, which is a challenge in the drylands of west Texas, says Marc Bianchi, analyst at Cowen. The two-lane roads of west Texas may not be able to handle fleets of sand trucks, he adds.

The majority of sand is sold on long-term contracts, industry executives say. Rising demand has stirred interest in expanding spot markets where miners, service companies and producers can swap loads and obtain more insight into prices.

PanXchange, a Denver-based company, this autumn launched an online frac sand exchange which it says now has nearly two dozen members including Hi-Crush.

The existing sand market is “very, very inefficient”, says Laura Fulton, Hi-Crush chief financial officer. “Having all this on a clearinghouse would really provide more transparency and more efficiency in the market, so you would know who has sand available to sell and what price they’re willing to transact at.”

The strengthening sand demand shows how oil wells have become more productive, according to Artem Abramov, who heads Rystad’s North America well research — so much so he believes that the “the market should not be surprised next year by an impressive 1.2m b/d of US light oil production growth”.