All Articles

PanXchange® Sand: Benchmarks & Analysis 06.26.2023

Interactive Charts Located Under Commentary

Frac Sand Market Commentary

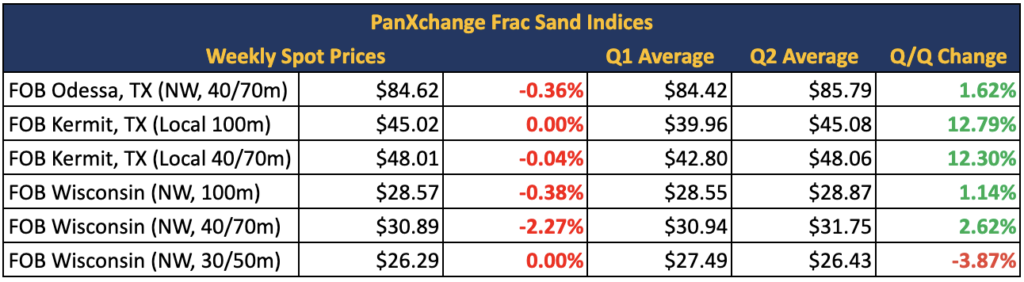

In the Permian basin, FOB Kermit 100m prices and 40/70m sand prices have fallen by $0.05 per ton respectively since last week, as they continue to bounce in the mid-40s per ton.

In the Northern White mine gate market, FOB Wisconsin 100m, 40/70m, and 30/50m sand prices have fallen by $0.10, $0.10, $0.00 per ton respectively since last week. While we continue to hear of a soft market for Northern White and relatively stable average spot pricing, there continues to be a wide range between high and low spot prices, with prices as low as $22 per ton and as high as $35 per ton at the mine gate.

The Primary Vision frac spread moved from 268 to 277 since last week, increasing for the third consecutive week. The Baker Hughes US rig count moved from 687 to 682, declining for the eighth straight week, suggesting that completion activity is focused on the drawdown of DUC wells. WTI prices were marked at $69.84 as of Monday’s open, notably dipping below the $70 per barrel mark.

US Energy Market Commentary

We continue to see a string of upstream M&A activity this week, as Civitas Resources announced on Tuesday its plan to purchase oil and gas operations in the Permian basin, managed by NGP Energy Capital Management, for $4.7 billion. This acquisition marks a significant expansion for Civitas, as it has operated exclusively in Colorado’s Denver-Julesburg basin until now. By entering the Permian basin, which is considered a lucrative shale industry hub, Civitas expects to increase its production by 60%. The agreement involves the acquisition of assets from Tap Rock Resources and all of Hibernia Energy III’s operations. One of its major shareholders, Kimmeridge, expressed support for the acquisition, highlighting the benefits of adding high-quality inventory and diversifying the company’s portfolio. In addition, this transaction is on brand for two key reasons. First, that the oil and gas industry is also sitting on relatively high amounts of free cash flow thanks to a greater commitment to capital discipline and higher oil prices. Secondly, the conservative approach to company growth has pushed operators to grow via acquisition as opposed to riskier exploratory drilling in new frontier regions. As the trend toward significant consolidation continues, PanXchange expects further consolidation of vendor contracts for oilfield services and proppant vendors to be on the horizon.

Frac Sand Supply & Market Share

To track any future mines that may come offline, interactive charts and graphics are shown below.