All Articles

PanXchange® Sand: Benchmarks & Analysis 09.18.2023

Interactive Charts Located Under Commentary

Frac Sand Market Commentary

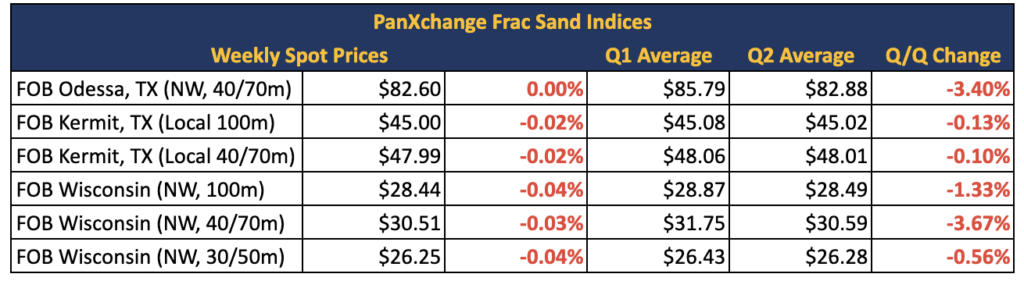

In the Permian basin, FOB Kermit 100m prices and 40/70m sand prices have fallen $0.05 each since last week.

In the Northern White mine gate market, FOB Wisconsin 100m, 40/70m, and 30/50m sand prices have fallen by $0.05 per ton each since last week.

Both Northern White and Permian Basin continue their soft-to-stagnant trend as crude oil pricing has held relatively stable and producers take a cautious approach to bringing new incremental production online.

The Primary Vision frac spread moved from 244 to 252 during the week of September 8. The Baker Hughes US rig count moved from 631 to 632 the week of September 8. WTI prices were marked at $88.75 as of Wednesday’s open.

US Energy Market Commentary

This week, we discuss the chaotic nature of oil and gas forecasting, and the effects on US oilfield services. While crude oil pricing has been largely stable through Q3 in 2023, the International Energy Agency (IEA) stated that the extended oil output cuts by Saudi Arabia and Russia until the end of 2023 will result in a significant deficit in the market during the fourth quarter. This decision by OPEC+ to limit supplies, which began in 2022, led to benchmark Brent crude surpassing $90 per barrel for the first time this year. Despite output cuts of over 2.5 million barrels per day by OPEC+ members since the start of 2023, increased supplies from non-alliance producers like the United States, Brazil, and Iran (which is still under sanctions) have balanced the market until now. However, starting in September, the loss of OPEC+ production is expected to create a substantial supply shortage in the fourth quarter, according to the IEA’s monthly oil report.

The IEA also highlighted broader economic concerns, particularly China’s slow post-pandemic recovery and worries about persistently high interest rates in the United States. Despite these concerns, the IEA noted that China, the world’s largest oil importer, has not been significantly impacted by its economic downturn so far. However, the agency cautioned that any sudden weakening of China’s industrial activity and oil demand could have global repercussions and create challenges for emerging markets in Asia, Africa, and Latin America. In sum, oilfield services vendors (including frac sand producers) continue to see soft-to-stagnant demand as crude oil pricing has held relatively stable and producers take a cautious approach to bringing new incremental production online.

Frac Sand Supply & Market Share

To track any future mines that may come offline, interactive charts and graphics are shown below.