All Articles

PanXchange® Sand: Benchmarks & Analysis 05.26.2020

Interactive Charts Located Under Commentary

Frac Sand Market Commentary

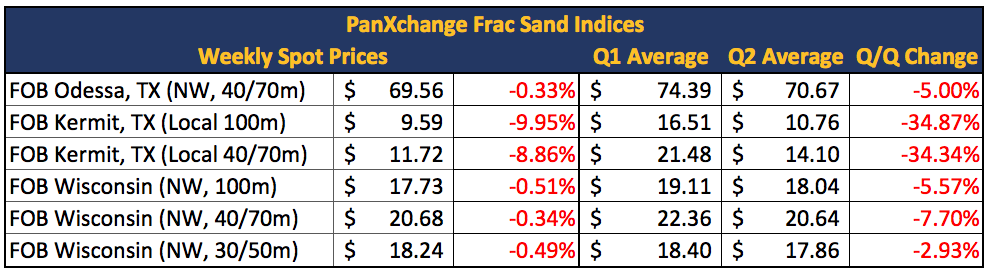

In the Northern White market, FOB Northern White Odessa 40/70m, as well as 100m, 40/70m, and 30/50m mine gate prices remained relatively stable, falling by less than 1% each this week across the board.

We continue to hear chatter from industry contacts that they are seeing far more stability in the Northern White markets versus in-basin supply, largely due more rig count and frac crew count stability in Northern-White-dominated regions such as the Marcellus, versus the activity centers in the Permian and Eagle Ford shale which predominantly use in-basin sand.

In the Permian, FOB Kermit 100m fell by 10% this week, while FOB Kermit 40/70m prices have fallen by 9% since last week. Net sand purchasers (E&P and oilfield services) continue to place pressure on frac sand producers in the region, as local 100m prices dipped below $10 per ton for the first time in history.

US Energy Market Commentary

This week, the theme of our commentary is the mitigation of risk amid uncertainty; an attractive prospect, especially given the recent upending of the market by the novel coronavirus.

In the futures market for both Brent Crude and WTI, barrels for December delivery have the highest open interest. This is unusual and likely demonstrates traders’ aversion to uncertainty surrounding near term contracts, especially after the long-squeeze on front-month WTI trading that led prices to an all-time low of negative $40.32 per barrel. Of note, the USO spread its exposure deeper into the future, having previously held its assets in one of the two front months of WTI futures.

As stated by IHS, the present energy market looks dire and we could see US production bottom out as low as 9 million barrels per day (previously peaked at 13 million barrels per day in February 2020). According to a recent article in the Wall Street Journal, “shale oil companies have sharply reduced their drilling budgets for the year, with the Top 15 by market capitalization slashing spending by an average of 48%”. A chief executive from IHS, one of the largest oil and energy data companies globally, was even quoted saying peak shale occurred in February 2020. Analysts at KPMG and Rystad Energy predict that at least 70-100 (or more) energy companies could face bankruptcy by year-end if prices do not recover fast enough to allow them to better cover their expenses, drill wells and maintain cash flow.

However, contrarians have cited that oil prices could rise quicker than expected. For instance, Mark Haefle, Chief Investment Officer at UBS was recently quoted in Business Insider saying “While the oil market is heavily oversupplied this quarter, we expect it to move toward balance next quarter and become under-supplied in 4Q this year as lockdown restrictions are eased and oil demand picks up.”

Regardless of the price outcome for crude, industry players like Harold Hamm, CEO of Continental Resources have learned the hard way that hedging price risk (be it on crude oil, natural gas, or even oilfield product input costs like frac sand) could be considered the energy industry’s most valuable commodity. He lost more than $3 billion of his net worth in a matter of days when crude prices first fell amid a battle for market share spurred by Russia and Saudi Arabia. His company, which he is a majority shareholder went into the oil price rout “naked”. In other words, unlike most energy companies, Continental Resources did not hedge the prices of the barrels they sell because financial instruments used for hedging can hurt profits in the event of a commodity price surge. As a result, Continental was forced to cut their overall production by approximately 70% by shutting in producing wells.

As of the end of the fourth quarter of 2019, approximately 43% of the 2020 US oil production was hedged, according to an analysis done by Goldman Sachs. While some hedges consist of a simple put option, which allows the energy company to sell their oil at a fixed price at a particular time, many shale producers used three-way collars. Three-way collars allow producers to make a “calculated bet that oil will fall to a certain level and no further” and redeem some of the cost of their hedge by selling put options below certain price levels. According to Managing Director Michael Tran from RBC Capital Markets, “Using many of these structures, producers are price-protected unless prices fall below a certain threshold, and $45 a barrel was a popular strike level, at which point producers become fully exposed,”.

It will be interesting to see how hedging will play a pivotal role for energy companies going forward, especially when faced with the potential of sustained low price levels for crude.