All Articles

PanXchange® Sand: Benchmarks & Analysis 10.23.2023

Interactive Charts Located Under Commentary

Frac Sand Market Commentary

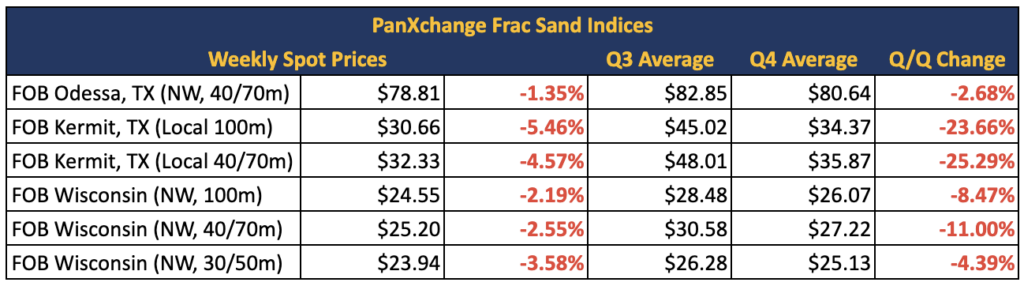

In the Permian basin, FOB Kermit 100m prices and 40/70m sand prices have fallen over $1.00 each since last week. Prices are responding to the softened demand for in-basin sand, especially as we have seen a significant drop in rig count and frac spread count since this time last year.

Meanwhile, in the Northern White mine gate market, FOB Wisconsin 100m, 40/70m, and 30/50m sand prices have fallen by $0.70 per ton each since last week.

The Primary Vision frac spread moved from 263 to 269 since last week. The Baker Hughes US rig count moved from 622 to 624 last week. WTI prices were marked at $88.00 as of Monday’s open. Despite WTI prices holding above the $85/bbl mark, producers have not yet substantially expanded drilling and completion activity.

US Energy Market Commentary

This week, PanXchange addresses this morning’s exciting news; Chevron reached an agreement to acquire its U.S. competitor, Hess, for $53 billion in stock. This deal exemplifies the strong desire of leading U.S. energy companies to secure oil and gas assets in a world where there is a growing focus on lower-risk future fossil fuel supplies and increased returns for shareholders.

This proposed transaction intensifies the competition between Chevron, the second-largest oil and gas producer in the United States, and its larger rival, Exxon. This move comes in the wake of Exxon’s rapid series of deals since July, including the acquisition of the top U.S. shale producer, Pioneer Natural Resources, and Denbury. These two acquisitions, with a combined value of nearly $64 billion, position Exxon as a dominant player in the U.S. shale market and solidify its presence in the emerging carbon storage sector. PanXchange views this transaction as setting a precedent for more consolidation transactions to come. To reiterate last week’s comments, The rebound in U.S. oil production amid high oil prices has led to considerations of repatriating oil production, as onshore shale is cheaper and less risky than offshore and international drilling. PanXchange expects consolidation of upstream customers, and improved production yield per well to be limiting factors for oilfield services vendors going forward.

Frac Sand Supply & Market Share

To track any future mines that may come offline, interactive charts and graphics are shown below.