All Articles

PanXchange® Sand: Benchmarks & Analysis 11.13.2023

Interactive Charts Located Under Commentary

Frac Sand Market Commentary

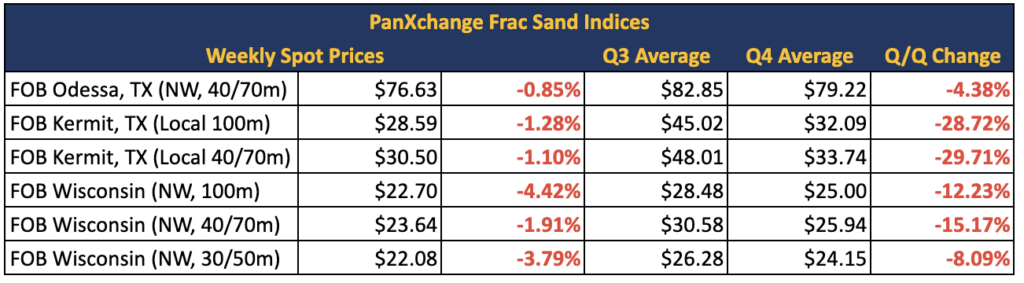

In the Permian basin, FOB Kermit 100m prices and 40/70m sand prices have fallen $0.30 each since last week. Prices are responding to the softened demand for in-basin sand, especially as we have seen a significant drop in rig count and frac spread count since this time last year (by 163 rigs and 27 frac crews respectively).

Meanwhile, in the Northern White mine gate market, FOB Wisconsin 100m, 40/70m, and 30/50m sand prices have fallen by $1.00, $0.30, and $0.30 per ton respectively since last week.

The Primary Vision frac spread moved from 270 to 268 since last week. The Baker Hughes US rig count moved from 618 to 616 since last week. WTI prices were marked at $77.15 as of Monday’s open as analysts respond to weaker-than-expected crude demand from China.

US Energy Market Commentary

Oilfield service companies focusing on U.S. shale oil and gas producers are expressing pessimism about fourth-quarter demand. Their upstream clients are being cautious with their spending as they have nearly exhausted 2023 budgets according to the analyst community. As many U.S. oil producers are maintaining flat production, redirecting more profits to investors, budgets broadly were not as large as they once were all else equal. In particular, shale gas producers have faced challenges throughout the year, struggling to reduce drilling quickly enough to counteract weak prices.This presents a gloomy outlook for service firms that have been grappling with increased costs for materials and labor for almost two years. Companies with significant international operations have a more positive outlook, but U.S. oil and gas producers are not eager to increase spending, according to industry executives. Despite hopes for a recovery, the reality in North America has not met expectations, as mentioned by Clay Williams, CEO of NOV Inc, the fourth-largest U.S. oil equipment and services supplier. Wall Street analysts have reduced profit expectations for North American-focused oilfield providers, with companies like NOV and Liberty Energy facing cuts in their fourth-quarter earnings estimates. ProPetro Holding, a competitor of Liberty Energy, may reduce its hydraulic fracturing fleet in the final quarter due to customers depleting their budgets. Analyst groups such as Rystad Energy anticipate a decline in active frac fleets in the U.S. during the fourth quarter. While some companies expect an uptick in demand early next year with new budgets in place, challenges such as flat production and recent mergers may keep drilling and completion services at lower levels. Recent acquisitions by Exxon Mobil and Chevron are expected to dampen demand in the near future as well, according to industry executives. By extension, PanXchange holds the view that frac sand vendors should expect a flat-to-lower demand environment heading into 2024.

Frac Sand Supply & Market Share

To track any future mines that may come offline, interactive charts and graphics are shown below.