All Articles

PanXchange® Sand: Benchmarks & Analysis 09.12.2022

Interactive Charts Located Under Commentary

Frac Sand Market Commentary

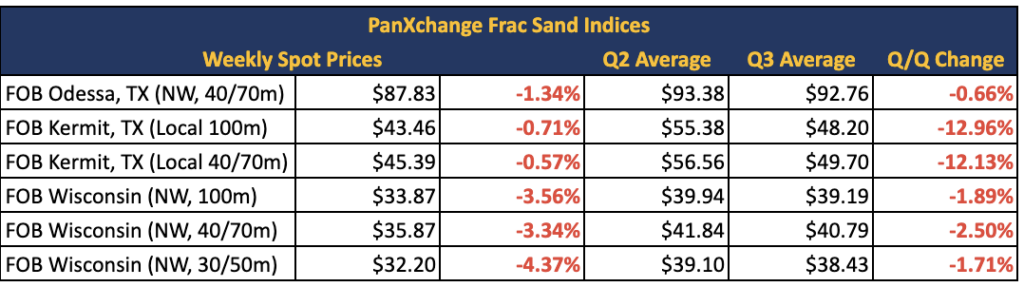

In the Permian basin, FOB Kermit 100m prices and 40/70m sand prices have fallen by $0.30 per ton respectively since last week, as average prices moved toward the $45 per ton range.

In the Northern White mine gate market, FOB Wisconsin 100m, 40/70m and 30/50m sand prices have fallen by over $1 per ton respectively since last week. As basins such as the Permian and Eagle Ford with in-basin supply have seen stabilized spot sand pricing with more balanced supply and demand stacks, there has been a drop-off in Northern White supply to fill the gap. As well, despite strong fundamentals ($10/MMBtu HH) in the Northern-white-dominated Northeast natural gas market (i.e Marcellus shale), we have continued to see limited growth in US frac spread counts, as operators continue to exercise capital restraint.

The Primary Vision frac spread moved from 282 to 284 last week. The Baker Hughes US rig count moved from 760 to 759. WTI prices were marked at $86.25 as of Monday’s open.

US Energy Market Commentary

This week, we discuss the implication of US natural gas futures hitting 14-year highs as a result of relentless demand for US shale gas in Europe, and the latest price spike due to Russia’s plans to indefinitely shut down the vital Nord Stream gas pipeline to Western Europe. While we continue to see strong demand for US natural gas for these reasons, we are not seeing a massive spike in rig or frac spread count as a result of capital discipline exercised by upstream producers, as well as export logistical limitations to Western Europe. While US natural gas production growth and the counts of rigs and frac crews do not correlate perfectly, production growth is consistent with the theme of capital discipline, particularly in the near term. Since May 2020, natural gas has held a fairly steady production climb of an average of 400-500 million cf/d each month according to EIA data. As well, this trend has held largely consistent with 10 year natural gas production growth data as well dating back to June 2012 suggesting an upper limit to monthly production growth as a result of capital discipline, production decline rates and other factors. In sum, PanXchange expects demand to intensify for US natural gas, and for this to provide strong fundamental support for in-basin Haynesville sand and Northern White sand delivered to the Appalachian gas region throughout the end of the year.

Frac Sand Supply & Market Share

To track any future mines that may come offline, interactive charts and graphics are shown below.