Africa News

Market Update: 12-19-18

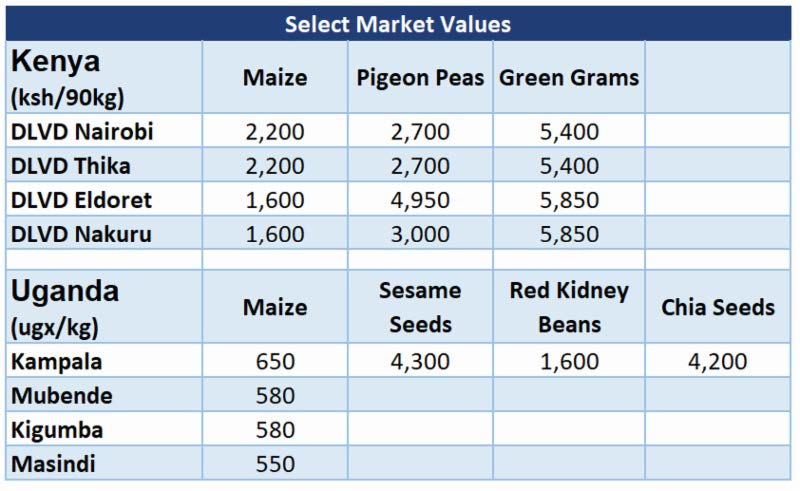

Kenya:

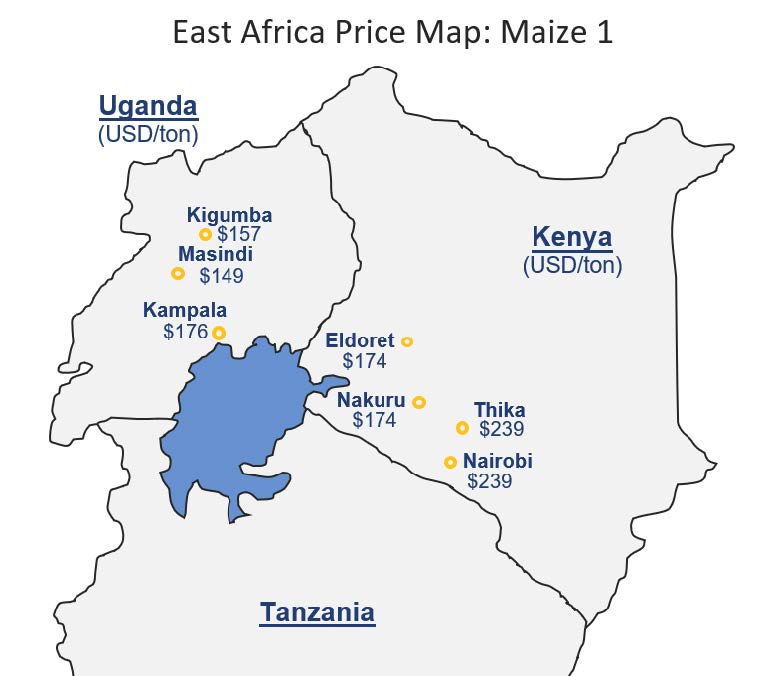

For the past two weeks, prices have remained relatively stable across the country and most commodities. Maize has continued to trade at Sh 2,200 per 90-kilogram bag in Nairobi and Thika, while prices have decreased slightly in Eldoret and Nakuru, trading at Sh 1,600 per 90-kilogram bag. The price of pigeon pea and green grams have been flat over the past two weeks, location specific prices can be seen below in the select market values table.

Per recent remarks from the Agriculture Ministry, it is becoming clear that there are hesitations to changing the price of maize originally set by the Strategic Food Reserve. Despite the recommendations from members of Parliament, Andrew Tuimur who serves as Chief Administrative Secretary, has stated that his hands are tied and is not able to alter prices. At the end of November, the Cabinet had approved the purchase of two million 90-kilogram bags at a price of Sh2,300 per 90kilogram bag.

Uganda:

The price of maize has remained consistent the past two weeks, trading at 650 UGX per kilogram in Kampala and 580 UGX per kilogram in Mubende, Kigumba and Masindi. While prices have been flat, a significant portion of the new crop will begin to enter the market during December, which should lead to prices decreasing going into the new year. Nambale beans and red kidney beans continue to enter the market in Kampala, mainly from the Mubende area, which should also lead to decreased prices in the coming weeks.

High value products such as sesame seeds and chia seeds continue to be in demand as the harvest period continues. Sesame seeds in Kampala are currently trading at UGX 4,300 per kilogram however a decrease in value is expected in the Lira area as the harvest fully integrates into the market. Most of the sesame seeds in the Kampala market are uncleaned, for any more information on cleaning requirements for grains and oilseeds please contact the PXAfrica team.

Additional details regarding the Genetic Engineering Regulatory Bill 2018 have been released, largely elaborating on the language that is included. A clause in becoming compliant with the Cartagena Protocol has been written in the bill, an international agreement aiming to ensure the safe handling, transport and use of living modified organisms (LMOs). All countries that have chosen to allow genetic engineering abide by the Cartagena Protocol, and should be received positively as it highlights the commitment to monitoring technologies and scientific innovations in the agriculture industry. The passing of the bill is largely seen as a positive due to the potential upside it brings to the industry, limiting the use of pesticides, reducing input costs and maximizing production.

Tanzania and International Markets:

The Tanzanian Ministry of Agriculture, on behalf of President John Magufuli, has been tasked with linking foreign markets with farmers to absorb the large surplus of maize within the country. As of right now, Tanzania has a four million tonne surplus of maize, and the figure is expected to grow to 20 million tonnes by the end of 2018. While Tanzania has local demand for about 13 million tonnes per year, and would like to keep about 200,000 tonnes as reserves, just shy of 7 million tonnes remains as surplus. According to the government, markets that are currently being targeted for exports are Kenya, South Sudan, Malawi and the Democratic Republic of Congo. Malawi has been reported to have set aside $27 million dollars to purchase maize.

Although strides towards a resolution in trade disputes between China and the United States are seemingly on the horizon, the effects of the trade war are impacting East Africa as China seeks alternative soybean sources. Prior to the trade disputes, China procured roughly 60% of its soybeans from the United States, and thus is searching to fill the void. Chinese importers are looking at East Africa as a potential source of soybeans, primarily used to make feed for the growing livestock industry in China, and have contacted companies in Rwanda as a potential source. Rwandan processors are largely operating under capacity, and import the raw beans from Uganda and the Democratic Republic of Congo in addition to using local supply. If the trade disputes between the United States and China are not resolved soon, this opens a greater opportunity for East African soybeans as an exported product.