Africa News

Market Update 08-15-18

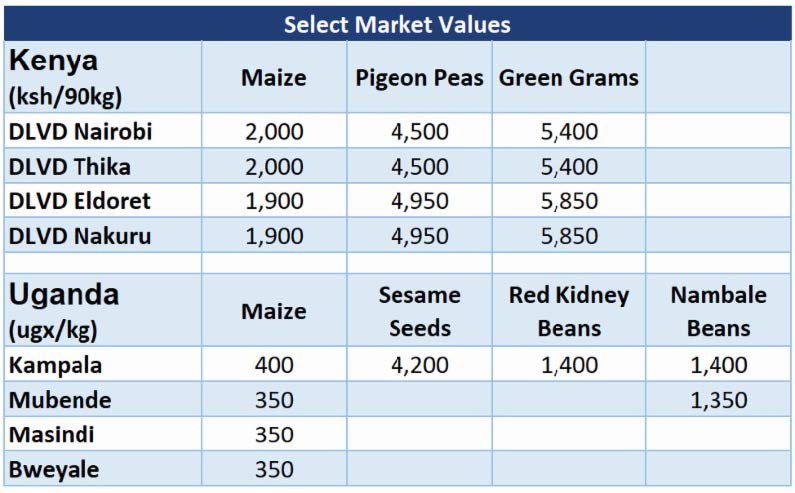

Kenya:

Kenya is facing a bumper harvest expected to put pressure on prices, particularly at the farm gate level. Exploitative politicians are predictably and preemptively blaming illegal imports from neighboring countries for price weakness ahead of the long rains harvest due to hit the markets soon, the likely outcome will be calls for increased government intervention. Farmers in Bungoma have again been complaining about middle men. The result will likely be continued calls for government support, arguably making the situation worse.

The NCPB has finally released Ksh 1.4 billion of the money owed to farmers from previous years’ deliveries to silos. With the NCPB warehouses in shambles, stores rotting, and financial situation worse yet, this seems like the wrong route. None of the cries have focused on underlying issues: lack of farmer cooperatives, an industry supported association enforcing contracts and creating standards, and localized, proper storage facilities. With these base facilities in place, farmer financing should naturally follow.

The East African Community has cleared 27 Kenyan manufacturers to import a total of more than 3 million tons of wheat from member states. Farmers are once again calling for protection.

Uganda:

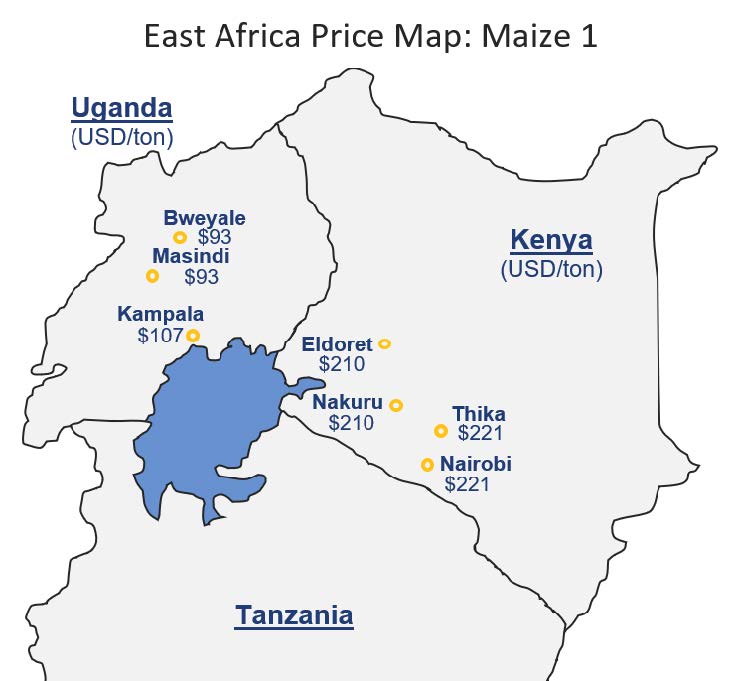

Maize prices have continued to decrease in Uganda, with some areas quoting UGX 200 per kg. This is primarily due to a bumper crop for the current harvest, with total production estimates approaching five million metric tons. The price of maize in the Kampala area is trading around UGX 400 per kg, while the Mubende area is slightly cheaper, trading at UGX 320 per kg. Due to the rapidly decreasing prices, the government has decided to intervene.

The vast majority of the Nambale beans are now dry, and do not require further machine drying. Currently, Nambale beans are trading at UGX 1,400 per kg. Sesame seeds are available at UGX 4,200 per kg in the Kampala area.

The article below is an excerpt from our Hot Commodities newsletter that goes out every other week.

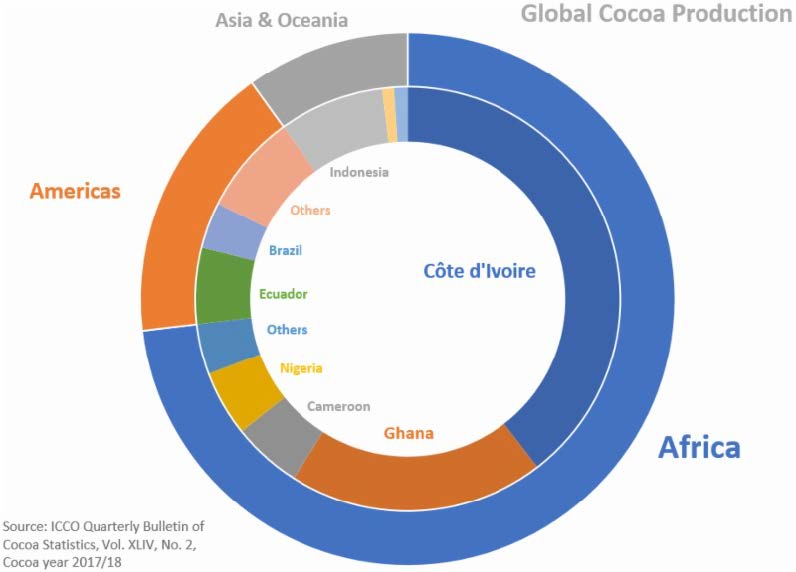

Deconsolidation in Cocoa Markets After a series of exits, bankruptcies, and subsequent fraud allegations (of) larger tradehouses in the cocoa space, smaller, more nimble shops are picking up the slack. The majority of cocoa is produced in Africa, with over half of the total global production in Côte d’Ivoire and Ghana. Smallholder farmers produce much of that total. (see aggregated production data below).

Physical trading in African nations is a tough endeavor, with few effective trade associations promoting rules and standards, and slow moving, ineffective, sometimes corrupt courts making contract enforcement difficult. Until these underpinnings of a formal trading environment develop, tradehouses must be able to work with farmers and traders in a volatile trading environment. Defaults and associated risks exacerbate price swings and cause trouble throughout the supply chain. These Wild West aspects of the cocoa markets are also reasons why margins are significantly better than larger commodity markets in developed nations.

While some of the majors are pulling out, other large traders with physical assets like grinding facilities still have a large market share; Cargill still grinds around 800,000 ton per year. Will this deconsolidation level the playing field, or just create a larger group of smaller buyout potentials?

The good news? Cocoa prices have fallen by over 20% since highs in April. 95% ultra-dark lovers shan’t worry about getting their fix.