Africa News

Market Update 09-26-18

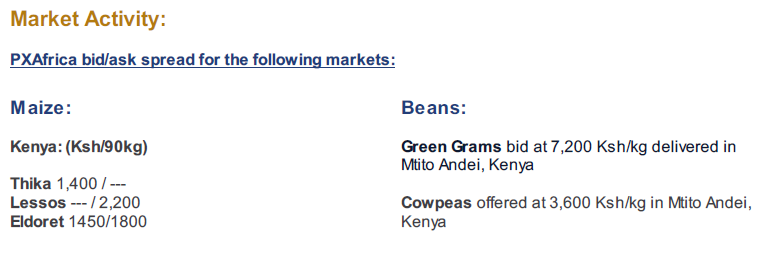

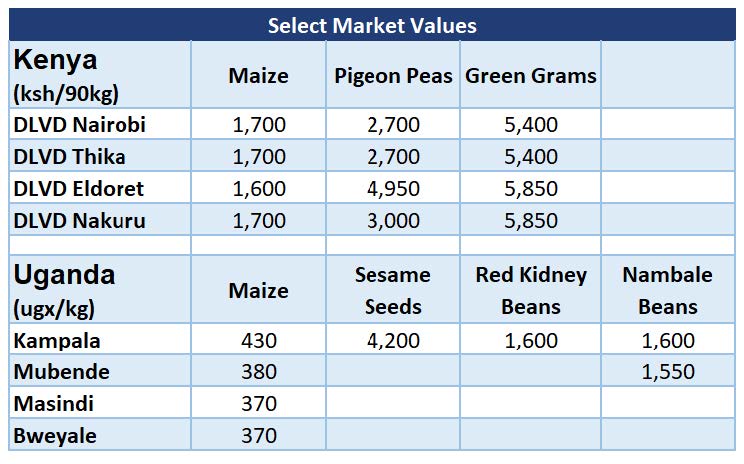

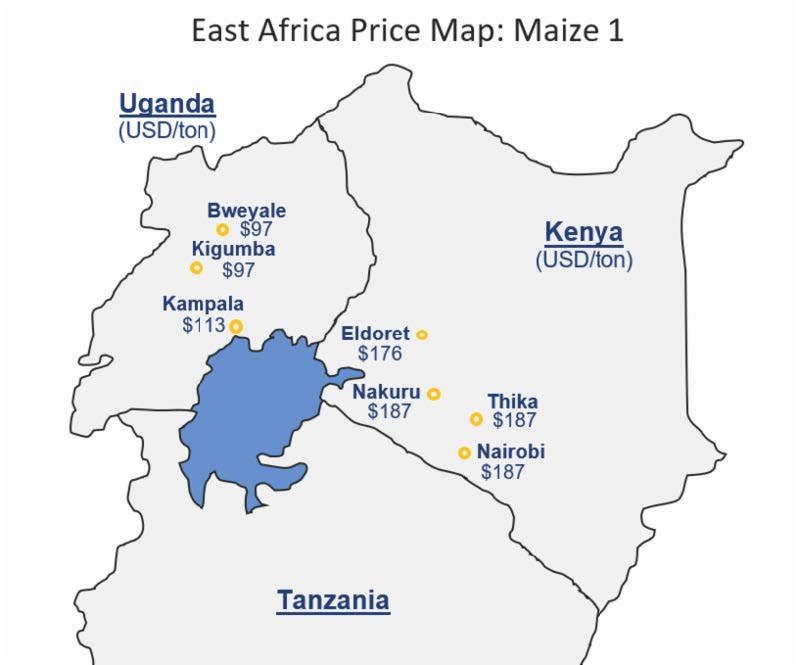

Kenya:

Farmers from the Eastern, Western and South Rift regions have started harvesting, but the peak period in the North Rift will be from next month until November. Farmers across the country are expecting a bumper harvest of 46 million bags of maize this season, a rise of around 30% year over year. Agriculture Cabinet Secretary Mwangi Kiunjuri said the harvest would be a welcome boost to the country’s efforts to attain food security. A bumper harvest unfortunately also has negative consequences for countries where such a large proportion of the nation is employed directly in the agricultural space. Farm-gate prices will likely see a ceiling through the end of harvest, and main markets will likely see Ksh1500 per 90kg by peak harvest time or sooner.

The NCPB could potentially be holding billions of shillings maize unfit for human consumption. Almost a million 90kg bags of maize estimated at Ksh3.1 billion bought as part of the strategic food reserve may be infected by the deadly aflatoxin, an internal audit report shows.

Uganda:

Maize trading at UGX 430/kg in the Greater Kampala area as the market continues to see high volumes. There are some concerns on the quality of the grain in the market as millers in Kampala have been rejecting parcels with small grain as opposed to the preferred big grain.

Red Kidney beans and Nambale beans trading at UGX 1,600 per kg in the Greater Kampala area. Prices are expected to increase before the market prepares for a new crop of beans in the December harvest.

Sesame seeds originating from Lira is available in Kampala at UGX 4,200 per kg. For high value seed or grain cleaning solutions please contact the PXAfrica team.

International:

Farmers across the U.S. are feeling the heat as the USDA estimates September soybean ending stocks of 845mm bushels, up from 60mm in August, and a whopping 300mm bushels over September 2017 (see chart). November futures settled below $8.50 per bushel, with cash prices across the U.S. equally as worrying. Delayed pricing service charges are up significantly year over year, and farmers without on- site storage anticipating better pricing in winter or spring will be at the whim of available storage space. Iowa, the second largest state agricultural economy in the U.S., will be hit particularly hard by the tariffs, with an Iowa State University analysis projecting Gross State Product (GSP) to lose $1 to $2 billion dollars due to the tariffs.

While U.S. prices (including the 25% tariff) have fallen enough to be competitive with what is still available from other origins, Chinese traders are hesitant to risk purchasing cargos and being ostracized by the government. The soybean tiff goes beyond just a tariff, and Chinese traders and particularly state owned enterprises will exhaust every available alternative even when US origin soybeans are economical with other origin prices.

One strategy discussed at an export conference by Mu Yan Kui, vice chairman of a trading subsidiary of Singapore based Wilmar International is to change hog feed rations from average 20% inclusion down to 12%. While commercial US feed operations build different rations based on regional commodity access, and least cost rations, US average of soy inclusion for hogs likely averages around 20%, but that’s largely due to availability of soybeans. European feed operations, which import a large portion of their soybean consumption, use a ration closer to 12%, with the balance made up of corn.

US Farmers aren’t shy to hardship, staying resilient through bumper crops and droughts, using risk management tools like futures and options contracts, integrating data like weather and satellite imaging. But the real question on farmers’ minds is what will be the long term damage. Chinese feed ingredient companies have been reluctant to switch to the lower soymeal rations, but this might accelerate the transition. China is already pouring billions into developing nations through the Belt and Road Initiative, and has the ins the easily transition into agriculture, in places like Kenya and Uganda with vast arable land but relatively low yields per acre. David MacLennan, CEO of Cargill, spoke of these long terms effects in a Bloomberg interview.

Markets are indeed dynamic. Winners and losers in a new market structure after the cooldown have yet to be chosen.