PanXchange® Hemp: Benchmarks & Analysis – July 2019

Spot Prices

Market Updates

Spot Market Updates:

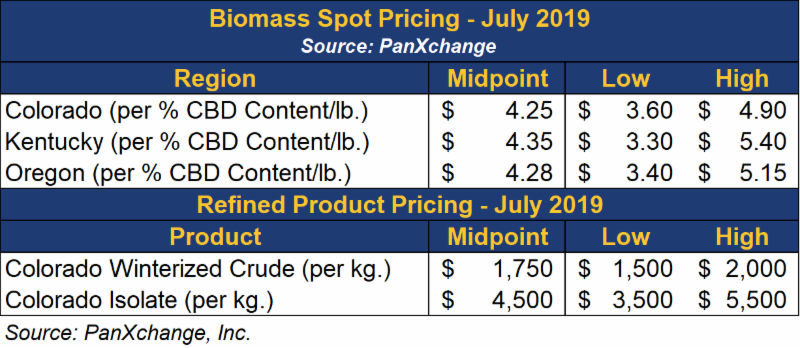

The spot biomass market throughout July has been transacting in the range of $3.30 to $5.40 per percentage point of CBD content (/point). As we move closer to harvest, an interesting trend is emerging as quality biomass is still available from firms that have held physical positions since the 2018 harvest. Prices on the high end continue to rise; however, PanXchange has seen an increase in lower-priced transactions over the past few weeks. Looking back at previous years, the old crop experienced large decreases in prices as the new crop entered the market. Farmers and firms who have played the carrying charge market are currently in a somewhat of a precarious situation, balancing risk and reward. On the one hand, the thought of missing out on profits could be motivation for taking below market value prices now and locking in profits. While on the other hand, there is still an opportunity, albeit an inherently riskier position, to catch upward trends of prices as biomass continues to become harder to find in the spot market between now and when harvest begins.

The Colorado crude oil markets have stabilized after consecutive months of downward pressure on prices. Winterized crude oil has been trading in the range of $1,500/kg to $2,000/kg, while non-winterized crude has continued to trade at a discount, generally in the range of $1,100 to $1,300.

The Colorado Isolate market has continued to be volatile and influenced by volume discounts as prices continue to come in slightly lower on a month-to-month basis. Overall, the Colorado isolate market has been transacting in the range of $3,500/kg to $5,500/kg in July.

Due to overwhelming demand, PanXchange is actively working to expand the data-points covered in our market assessment to include additional products and locations for the price indices. For more information on this project, please reach out to the PanXchange staff at hemp@panxchange.com

Cultivation Update:

Comments from within the PanXchange network have reported positive remarks and that crops are doing well looking towards the 2019 harvest, particularly in states like Colorado, Kentucky, and Tennessee. We are currently in the downturn of a strong heatwave affecting Colorado, the Southeast and the Northeast which can lead to plant stress on a maturing crop; however, a reprieve from the excessive heat in much of these areas will give the crops a chance to recover. In addition to the warm weather, Hurricane Barry was the first hurricane to hit the United States this season. The storm hit Louisiana as a Category 1 hurricane before quickly weakening to a tropical storm and bringing significant rain and flooding to Arkansas, Missouri, Illinois, Indiana, and parts Kentucky before continuing east.

Due to a lack in availability of hemp specific data in circulation, we are again looking at the USDA Crop Progress report which covers traditional agriculture crops such as corn, soybeans, barley, and cotton. While hemp is indeed a unique crop from a cultivation standpoint, the data from the report serves as a proxy for expected crop health. According to the data distributed on July 22nd, farmers in major hemp producing states have reported predominately good crop condition. More specifically, the only two states highlighted in the table below that have over 10% listed as less than ideal conditions are Wisconsin and North Carolina. Although corn is not a perfect comparison for hemp, the forecast is still noteworthy.

Soil conditions in major hemp producing states also look conducive for good growing conditions. Many of the hemp producing states are showing predominantly adequate soil conditions; however, Oregon and North Carolina are on the dry side while Wisconsin and New York are showing signs of surplus moisture. With proper field preparation (drainage and irrigation), these conditions are not alarming but a trend worth watching when looking at potential impacts to crop yields as harvest approaches. Another trend to note as we near closer to harvest is that the planting of hemp has continued throughout July. While delays in planting can be linked to a lack of accessible seeds and clones in the market and adverse weather patterns, each day that planting is delayed ultimately increases the chance that frost and hail can impact potential yields.

Additional Value Extraction:

A preemptive apology to you guys at the hemp conferences with the “We buy spent biomass” shirts. We’re stepping on your toes a bit today. While the main focus for this harvest season will be from CBD streams, stakeholders along the entire supply chain would be prudent to start looking at ancillary streams for value extraction, including smokable hemp flower, spent biomass, and hemp stalks.

Smokable hemp flower

Separating and trimming hemp flower gives producers the option to create a high value, niche product that could create additional revenue for producers who have the labor to allocate to these specific activities. Sales channels for smokable hemp flower market are closer to a retail product than an industrial commodity, however, with high-quality flowers retailing for over $1,000/lb throughout the country, the incentives are prominent for farmers to entertain exploration.

Beyond looking at the smokable hemp market as an additional revenue stream, a series of bills are currently circulating throughout state governments in Indiana, South Carolina and North Carolina regarding the legality of the possession, sale, and consumption of smokable hemp flower. These bills have the potential to impact this emerging market. Law enforcement has stated that smokable hemp and marijuana are indistinguishable based on smell and looks, thus making critical decisions more difficult as adequate training on this topic has not been provided, and many field tests only decipher the presence of THC rather than the concentration being greater than three-tenths percent. In addition to law enforcement, it remains to be seen what will come of the proposed legislation, and to what extent the tobacco lobby is playing due to both North Carolina and South Carolina being two of the largest tobacco producers in the country. A ban in these states would not only impact farmers who have invested money into cultivating smokable hemp this year but would also add to the confusion of state laws differing dramatically throughout the country.

Spent Biomass:

Animal Feed:

The first use of spent biomass will likely be for use in animal feed. Being heavily composed of cellulose, spent biomass will be used for feeding ruminants and partial-ruminants, and there will need to be regulatory clarity from USDA as well as state agencies before approval can be granted for feeding as hemp products are still not approved for use in animal feed ingredients. Colorado started a research program two years ago for spent biomass, but the Colorado Department of Agriculture (CDA) still lists no approval for use in commercial animal feed.

On the CDA website, the following statements have been made about the use of industrial hemp in animal feeds. “Currently, industrial hemp is not an approved ingredient for commercial feed. The use of an ingredient or feed additive that is not pre-approved can result in the feed being considered adulterated and not allowed for distribution in Colorado or other states.” Further, the CDA stated that the, “CDA does not approve registration applications for commercial feed products that contain industrial hemp since it is not an approved ingredient recognized by the Association of American Feed Control Officials (AAFCO, an organization of state agriculture departments from all 50 states) or the US Food and Drug Administration (FDA) Center for Veterinary Medicine.”

Cellulose Biofuels:

We’ve also heard and have had several inquiries about hemp for cellulose ethanol production. Because hemp plant matter has extremely high cellulose content, using it as a feedstock for ethanol could be another valuable application. But the economic viability of cellulose ethanol has yet to be shown on a significant scale as extensive research and development is required.

Paper:

In addition to feed and biofuel applications, additional secondary markets such as hemp paper have begun to enter the market due to relatively low barriers to entry. In some cases, hemp processors have entertained removal of spent biomass for free or at little to no cost, which has enabled these companies to cut costs associated with research and development and increase scales of operations.

Hemp Stalks:

Most of the CBD strains currently approved for production are bred with genetics conducive to oil production and not necessarily fiber. Producers and processors vying to strip the flowers and leaves off of the main stalk to produce a shucked biomass should at least explore the opportunity and viability of using the stems for fiber and hurd production. These two applications have received significant media attention as of late, but commercial scalability is still in early stages.

Fibers for Textile Production:

We’ve had a handful of conversations about a market for hemp fibers as an ancillary value stream. The commercial scalability of companies currently producing textiles from hemp fibers won’t be able to handle the volume, and vast variation from many farmers brand new to the plant. While this is certainly a long term proposition, for this year, producers could start to explore the potential for partnerships with fibers, but significant value add could be challenging.

Hemp Hurds (shivs) for Hempcrete:

Hemp hurds or shivs contain a high amount of silica, unique to the hemp plant, allowing them to bind with lime to produce a lightweight, high insulation value construction material, and has been used in Europe, particularly France, for many years. Hemp hurds are likely in the same position as fibers.

In the early days of these ancillary value streams before efficient markets develop, building early relationships around additional value streams could pay off in the long term. While there might not be the same immediate value that the CBD aspect of the industry will bring, spent biomass is likely to be the most viable in the near term as it will be widely available due to increases in processing capacity throughout the country. Fibers and hurds have potential, but because commercial scalability on the buy-side has been slow, and the huge variation in the supply stalks, these markets are likely to develop over time.