The frac sand market continues to be action-packed heading into this week. The Permian is experiencing substantial difficulties related to the unprecedented cold weather snap that has extended to the southern reaches of the United States. Prices have largely held flat as deliveries and sand plant operations have stalled due to the inclement weather. Plants have lost power and having plant equipment freeze-up has left sand producers with limited options until they are presented with better weather this week and have their power supply restored. In the Permian, FOB Kermit 100m and 40/70m sand prices decreased by $1.00 and $0.70 per ton respectively since last week, as producers have increased capacity to produce in-basin sand. However, prices still remain at highs not seen since the frac sand price surge in February 2020.

The frac sand market is off to an explosive start in February. In the Permian, FOB Kermit 40/70m and FOB Kermit 100m frac sand prices have leveled off since last week’s massive gains, falling by $0.75 and $1.40 per ton respectively since last week. Even with the leveling off in prices, they are still at highs not seen since February 2020. The Permian producers continue to race to catch up to growing demand. Chatter coming from various producers of expanding plant capacity in the region appears to have placed downward pressure on prices.

Major wheat exporter Russia announced the introduction of a duty for the export of wheat at 25 Euros per ton (KES 3,225) due to the shortages in the country and a move to stop domestic prices for bread from increasing. This intervention by the government in Moscow will hurt Kenya’s imports and has already has seen the price of bread on shelves increase.

The frac sand market is off to an explosive start in February. In the Permian, FOB Kermit 40/70m and (in particular) FOB Kermit 100m frac sand prices have accelerated their upward climb, increasing by $3.00 and $6.00 per ton respectively since last week. Prices in this range have not been seen since the frac sand price surge in February 2020. The Permian is experiencing a temporary shortage of in-basin supply as producers race to catch up to growing demand, bolstering prices in the near term. There has been chatter coming from various producers of expanding plant capacity in the region. Frac sand’s rapid demand recovery has led to an acute shortage of trucking and last-mile logistics options in the near term and has exacerbated the increase in frac sand prices. Meanwhile, FOB Odessa Northern White 40/70m prices fell by $0.25 per ton since last week. Capital expenditures using in-basin sand (all else equal) are more likely to be economic at current crude oil price levels than a more expensive completion design utilizing Northern White sand. As a result, in-basin prices are rising, while NW Odessa prices continue their downward trend.

As we illustrated in last month’s year-end report, the cannabinoid market is grossly oversupplied. Not surprisingly, producers throughout the country continue to struggle with spot transactions and selling products outright that were not contracted for 2020. Processors continue to reiterate that the quality of the product varies widely with newer, inexperienced growers. Trading has been light this month, yet the bottom on biomass pricing continues to decline, consolidating around a low of $1/lb. This consolidation creates an imminent problem considering that processors are charging anywhere from $1-5 per pound for outright processing on biomass, far more than the product itself is worth. Nonetheless, due to product degradation, many producers were forced into processing agreements to avoid further degradation of unsold biomass.

The first several weeks of 2021 in the world of frac sand have been action-packed. In the Permian, FOB Kermit 100m and FOB Kermit 40/70m frac sand prices have continued their upward climb, increasing by $0.65 and $3.00 per ton respectively. The Permian is experiencing a temporary shortage of 40/70m supply as producers race to catch up to growing demand, bolstering prices in the near term. However, we expect that the price spread between 100m and 40/70m local in-basin sand will narrow within a several week time frame as more 40/70m supply comes online. Meanwhile, FOB Odessa Northern White 40/70m prices fell by $0.50 per ton since last week. Capital expenditures using in-basin sand (all else equal) are more likely to be economic at current crude oil price levels than a more expensive completion design utilizing Northern White sand. As a result, in-basin prices are rising, while NW Odessa prices continue their downward trend.

Kenya has seen an increase in the local bread price as a result of the increased price of milling wheat in the global market that has seen the grain’s price level reach KES 33,000 per metric ton from KES 25,300 per metric ton and this has seen a 400 gram loaf of bread increase from KES 50 to KES 55.

It has been another action-packed week in the world of frac sand as we have seen substantial price changes in both the Permian and Northern White Sand markets. In the Permian, FOB Kermit 100m and 40/70m prices have risen by $1.25 per ton and $1.75 per ton respectively.

It is an exciting week in the world of frac sand, as prices have become increasingly volatile in the new year. In the Permian, FOB Kermit 100m and 40/70m have risen by $0.50 per ton each, after an expected increase in budgetary flexibility, increase in crude oil prices, and increase in trend towards tighter frac stage spacing and increased unconventional lateral well lengths (on average). FOB Northern White Odessa 40/70m prices increased by over $2 per ton last week ( an increase of 3%).

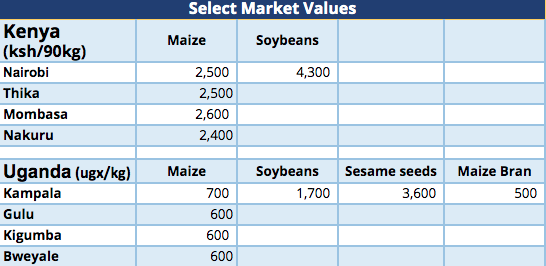

The National Cereal and Produce Board (NCPB) in Kenya has opened its depots and started buying maize with a targeted price of KES 2,500 per 90 kg bag which is slightly higher than the prices that traders were paying in the region of KES 2,200 and KES 2,300.